India's Leading Loan Distribution Company Offering Instant Free CIBIL Score Check Online

Instantly check your CREDIT score with Prime Loan, India’s leading loan distribution company. Enjoy a seamless experience as you access your credit score for free and get a detailed credit report. Whether you’re exploring loans, insurance, or tracking your financial health, Prime Loan is your trusted partner on the path to financial stability and success.

What is the CIBIL Score?

A CIBIL score represents your creditworthiness, calculated from your credit history and financial behavior. Ranging from 300 to 900, a higher CIBIL score signals better credit health. Financial institutions use this score to assess lending risk. A good CIBIL score can unlock favorable interest rates and loan terms, while a lower score may result in higher interest or loan rejections.

Importance of Checking Your CIBIL Score Online

Regularly checking your CIBIL score allows you to monitor your financial standing, catch any inaccuracies, and take steps to improve your score if needed. With convenient CIBIL score check online options, staying informed is simpler than ever you can get your CIBIL score online with just a few clicks.

CIBIL Score Range and What it Means

In India, the CIBIL Score ranges from 300-900 and is further divided into several categories:

|

CIBIL Score

|

Creditworthiness

|

|

|---|---|---|

|

550 and below

|

Bad

|

You have a low chance of getting a loan, especially for a high amount. Discipline your finances before applying for a loan.

|

|

550 - 649

|

Poor

|

Delayed loan payments reflect the risk of not paying a loan on time. Improve your score by paying previous loans before applying for new ones.

|

|

650 - 699

|

Average

|

Loan approval is possible but with higher interest rates and fewer benefits. Improve your score by making timely payments.

|

|

700 - 749

|

Good

|

With a good CIBIL Score, your chances of loan approval increase. Further, improve your score to get better interest rates.

|

|

750 - 900

|

Excellent

|

This score indicates timely payments. Borrowers with super CIBIL Scores are considered low-risk and can get high loan amounts at attractive interest rates and minimal paperwork.

|

How to Check Your CIBIL Score for Free at Prime Loan : Simple Steps for an Instant CIBIL Report Online

Check Your CIBIL for Free with Prime Loan. Follow these simple steps:

Go to Check CIBIL Score : Visit Prime Loan website and go to ‘Check CIBIL Score.

Sign in with Mobile Number : Enter your mobile number to sign in.

Fill out the Form : Enter your details, including your PAN number.

Get Your Score : View your CIBIL score instantly for free.

To monitor your credit health, you can check CIBIL score online for free with Prime Loan. With our Free CIBIL Score option, you can view your CIBIL report free, providing a comprehensive look at your credit profile. For a smooth experience, try our CIBIL check online and explore the advantages of online CIBIL score options.

How to Check Your CIBIL Score for Free at Prime Loan : Simple Steps for an Instant CIBIL Report Online

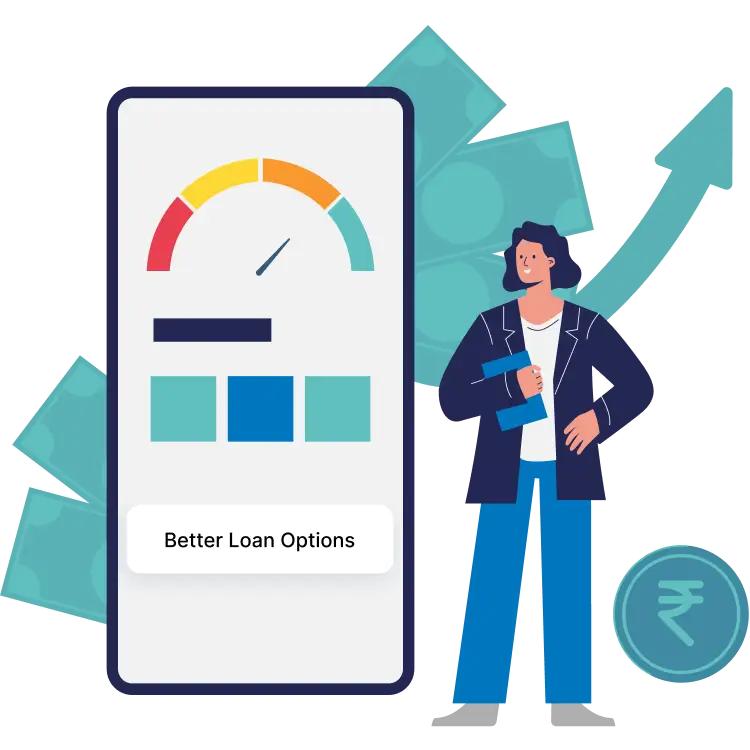

Easy Loan Approvals

Higher chances of loan approvals from banks and financial institutions.

Better Interest Rates

Access to loans at more competitive interest rates.

Higher Credit Limits

Eligibility for higher credit limits on credit cards.

Faster Loan Processing

Quicker processing of your loan applications.

How Prime Loan Helps You Manage Your CIBIL Score

Managing your CIBIL score is effortless with Prime Loan by your side. Offering free CIBIL Score Checks and expert advice, Prime Loan helps you monitor, manage, and improve your credit score effectively. Whether you’re seeking loan products, mutual funds, or insurance, our extensive network of 275+ private banks, PSU banks, NBFCs, and financial companies ensures you get the best options tailored to your needs. With Prime Loan , you not only access financial solutions but also gain the tools to build a stronger credit profile. Empower your financial future with Prime Loan the partner you can trust for smarter financial decisions!

Tips to Improve Your CIBIL Score: Expert Advice and Free Online CIBIL Score Check by PAN Card

To boost your CIBIL Score, Consider the following strategies:

Pay On Time

Pay your bills on time. Late payments can hurt your CIBIL Score. Set up auto payments or reminders for due dates.

Manage Credit Utilisation

Use less than 30% of your total Credit across all cards. Low balances compared to your credit limit show lenders you manage your Credit well.

Diversify Credit

It’s good to have a mix of different types of credit accounts, like Revolving Credit (credit cards) and Installment loans (auto loans, personal loans, mortgages).

Keep Old Accounts

Age of credit history matters. Older accounts contribute to longer credit history and better score. Think twice before closing old accounts which can shorten your credit history and increase your utilization ratio.

Monitor CIBIL Score

Monitor your Cibil Score and report through credit bureaus or third-party apps. By monitoring your score you can know the impact of your financial activities on your score and prevent identity theft.

Check Credit Reports

Check your credit reports regularly for errors or fraud. Dispute with the credit bureau and lender if you find errors.

Use Secured Credit Cards

If you are building Credit from scratch or repairing Bad Credit a secured credit card can be a good option. The credit limit of these cards is determined by the amount of cash you deposit. Pay the balance monthly to establish a good payment history.

Seek Professional Help

If you need more time to improve your Credit, consider consulting a credit counselling service. In addition to providing personalised advice, they can set up a debt management plan for you.

Apply for Credit Sparingly

Every time you apply for Credit a hard inquiry is made which can temporarily lower your score. Apply for new Credit sparingly and as needed to avoid multiple hard inquiries in a short span.

FAQs

A credit score is a 3-digit number (between 300 to 900) calculated by the credit bureau using the credit history of the individual.

Banks and NBFCs (Non-Banking Financial Companies) have to share the credit history of their customers with all four credit Bureaus.

The credit history of an individual consists of credit amounts, lender names, loan and credit card limits, loan EMI and credit card bill payment records, any default on a credit card account, personal details, etc.

This may happen due to the following reasons:

- Credit score from two Credit Bureaus would be different. There are four RBI authorised Credit Information Companies (CIC) in India : CRIF High-mark, Experian, Equifax and Transunion (CIBIL). Each Bureau has its own proprietary mechanism to calculate your Credit Score

- Credit scores fetched from the same bureau but on different dates can also differ.

You can build your credit score in 4 steps:

- Use only 50% of your credit card limit a month.

- Pay all your loan-related dues on time.

- Use credit cards regularly based on your requirements.

- Make timely payments of your credit card bills or EMIs.

A credit report is a statement of all the loans and credit card history of an individual reported to a credit agency by lenders – Banks & NBFCs. Credit card history is data that has all the information about the current credit status such as credit card payments, loans, etc.

Having a good credit history gives you the benefit of creditworthiness with helps you to avail loans seamlessly.

Following are the prominent factors you must consider to manage a good credit score:

- Repayments of credit card bills and loan EMIs on time.

- Utilization of credit card limits.

- Duration of credit cards and loan amounts.

- Total number of credit cards and loan amounts.

- Balance between secured and unsecured loans.

- Settlement status of credit cards or loan amounts.

A credit score is a three-digit number, which represents your entire credit history of all kinds of loans and credit cards.

A credit information report (CIR) consists of all your loan and credit cards related information.

Below are the common factors that can affect your credit score:

- Payment history speaks a lot about how you've maintained your repayments. Delayed, late, or incomplete payments over your credit card and loan can affect your credit score negatively.

- Credit utilization ratio is a ratio of credit that is being used. More than 40% credit use indicates increasing payback stress, which can negatively affect your score.

- Lenders consider having a variety of loans. Maintaining a balance between loans and unsecured loans can have a positive impact on your credit score and vice-versa.

- Through the length of your credit history, the age of your credit is calculated. Having a long experience in managing credits represents a better score.

- Too many inquiries or credit accounts that you've created can indicate risk and can hurt your credit score. Such situations are also called hard inquiries that allow lenders to access your credit reports.

Your credit score and credit report are updated regularly, typically whenever new information is reported to the credit bureaus by your creditors. This can vary depending on the creditor, but it's common for them to report to the credit bureaus every month.

In general, your credit report will be updated as soon as new information is reported to the credit bureaus, which could be as frequently as daily or weekly.

However, it's important to keep in mind that not all creditors report to all three major credit bureaus (CRIF-Highmark, Equifax, Experian, and TransUnion-CIBIL), so your credit report may not be identical across all three bureaus.

Your credit score, on the other hand, is calculated using the information in your credit report at a specific point in time. So while your credit report may be updated frequently, your credit score will generally only change when a new credit report is pulled and your credit score is recalculated. This could happen, for example, when you apply for a new loan or credit card.